South African Market Commentary: April 2026

Domestic rotation supports SA market gains

South African markets delivered modest positive returns in April, supported by improved domestic sentiment, rand strength and a rotation toward locally oriented assets. Equities advanced, led by financials and industrials, while resources declined as gold equities pulled back after prior-month outperformance. Small caps outperformed across market capitalisation segments, and domestically focused industrial and logistics counters were among the strongest individual performers. Fixed income markets strengthened as nominal yields declined, while listed property continued its recovery. The rand appreciated against the US dollar, supported by broad dollar weakness and firmer commodity prices. Inflation edged higher but remained within the SARB’s revised tolerance band.

Key highlights:

- South African equities gained as financials and industrials led market performance.

- Fixed income and listed property strengthened as nominal yields declined.

- The rand appreciated, supported by broad US dollar weakness and improved emerging market sentiment.

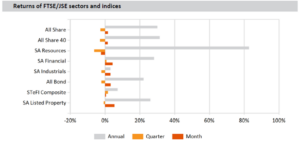

South African equities delivered modest positive returns in April, with the FTSE/JSE All Share Index gaining 1.7% and the Capped All Share Index also rising 1.7%. In terms of market capitalisation, the Small Cap Index outperformed, rising 3.5%, followed by the Top 40 Index, which advanced 1.6%, while the Mid Cap Index rose 0.9%. Sectoral performance was led by financials, which advanced 4.3%, reflecting positive sentiment toward domestic income-generating and rate-sensitive assets. Industrials gained 3.2%, supported by improved domestic risk appetite and rand strength which benefited import-exposed businesses. Resources declined 2.3% over the month, weighed by a retreat in gold equities despite elevated bullion prices, as the sector partially reversed the prior-month’s outperformance. Overall market performance reflected a rotation from commodity-linked rand-hedge counters toward domestically oriented financials, logistics, and industrial businesses.

Among notable individual equity movers in April, Montauk Renewables was the standout performer, rising 33.7% over the month. Logistics group Grindrod advanced 19.7%, and KAP Industrial Holdings gained 19.1%, reflecting improved sentiment toward domestically focused industrial and logistics businesses. On the downside, coal producer Thungela was the weakest performer, declining 13.4%, reflecting ongoing pressure on coal prices and export volumes. Afrimat fell 11.1% and Mondi declined 9.4%.

South African fixed income markets performed strongly in April. The All Bond Index gained 3.3% as nominal yields declined across the curve, reflecting lower global risk premia and improved domestic sentiment. Inflation-linked bonds advanced 4.3%, while STeFI cash returned 0.5% for the month. Listed property continued its recovery, with the FTSE/JSE All Property Index surging 5.8%, supported by lower long-end bond yields and improved domestic growth expectations.

The South African rand strengthened 2.4% against the US dollar during April, closing at R16.70 per US dollar. The rand’s appreciation was supported by broad US dollar weakness, firmer commodity prices, and improved emerging market risk appetite. On a year-to-date basis, the rand remained marginally weaker against the US dollar, reflecting the volatility experienced during the first quarter of 2026.

South African consumer price inflation edged higher in March 2026. Headline CPI rose to 3.1% year-on-year from 3.0% in the prior month, remaining comfortably within the South African Reserve Bank’s revised 2%-4% target band. On a month-on-month basis, headline CPI rose 0.6%. Core inflation, which excludes food, non-alcoholic beverages, petrol, and energy, rose to 3.2% year-on-year from 3.0% previously. Key contributors to headline inflation included housing and utilities, and insurance and financial services.

On the producer side, South Africa’s producer inflation (PPI) rose to 2.3% year-on-year in March 2026 from 1.8% in February, driven primarily by gains in food, beverages and tobacco, alongside continued strength in furniture and broader manufacturing. Additional upward pressure came from non-metallic minerals, electrical machinery, and transport equipment, while the drag from coal and petroleum products eased. On a monthly basis, PPI increased by 1.1%, the strongest rise in a year, signalling a modest reacceleration in upstream price pressures.

South African Market Indices Performance

About the South African Market Commentary

The retrospective RisCura South African monthly Market Commentary, offers investors insights across key segments including the local markets and economic trends to gain clarity on economic indicators, asset performance, and market dynamics. Geared for informed investors, our insight into emerging markets empowers strategic decision-making in the dynamic South African market.

Subscribe to the South African market commentary by RisCura to understand the economic indicators and factors that affect the economy.