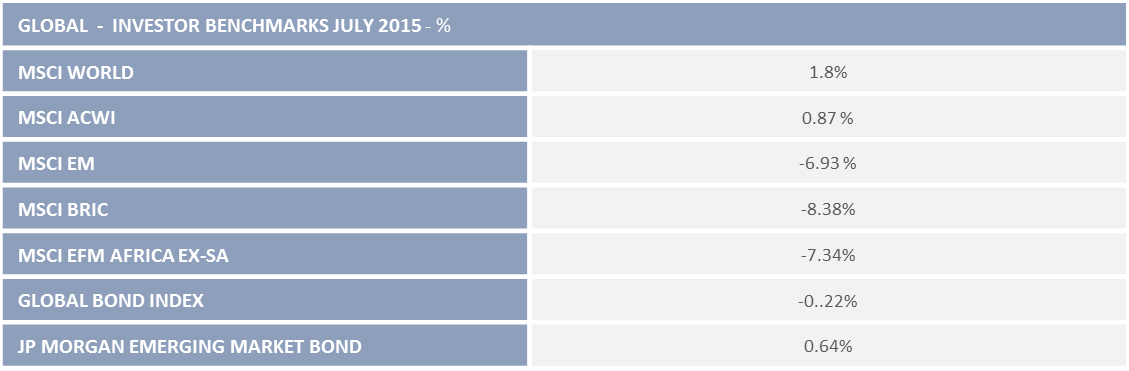

Global equity markets were marked by the distinct divergence between developed and emerging market performance. US, UK and Eurozone markets rallied after a dismal June, aided by the interim resolution of the Greek debt crisis and sound home-country data. Emerging counterparts, however, suffered severe backlash from developments in China (both its stock-market seesaw and growth slowdown), the slowdown in commodities and the imminence of US Federal Reserve Bank tightening.

US Markets

US equities ticked up nicely during July: the S&P500 gained 2.1%, the NASDAQ closed the month 2.84% higher and the Dow gained a more moderate 0.52%. July saw the release of some sound economic data, underpinning the overall view that the States is on track to achieve an overall 3% GDP growth rate for 2015. Second Quarter growth was reported as 2.3% and, more encouragingly, First Quarter figures were revised upward (from a -0.2% contraction to a 0.6% expansion). The good news is trickling through to consumers’ and producers’ spending patterns: Personal spending rose by 0.9% in May, and an estimated 0.2% in June, and the Department of Commerce reported that household spending had increased by 2.9%. While durable goods orders jumped by 3.4% month-on-month, the somewhat more pedestrian increase of 0.9% (with the exclusion of the volatile aircraft and defence sectors) is on par with the general trend in capital expenditure. The US Flash Purchasing Managers’ Index (PMI) was recorded at 53.8 for July.

Purchasing Managers Index figures above 50 an economy or sector in expansion.

Despite the still-surging Greenback, US exports increased by 5.3% in the 3 months to June, nearly a reverse of the First Quarter’s -6% contraction. Data on the housing front was mainly positive. Median house-prices increased by just under 5%, per the Case-Shiller Housing Price Index. Housing starts were 9.8% higher, to reach an 8 1/2 year high. While existing home sales’ numbers were well above expectations, new home sales fell to the lowest level in 7 months. The somewhat contradictory data is perhaps telling of a still-wary US consumer – a wariness underscored by recent sentiment surveys. The Conference Board and University of Michigan both reported ebbing consumer confidence, with the University of Michigan measure declining to 93.1 in July. Retail sales figures from June (at -0.3%) were particularly weak. Whilst employment data has been largely positive, the Federal Reserve Bank has noted that it would like to see “some further improvement”. Headline unemployment has consistently declined in the US. The addition of 223 000 jobs in June, and a respectable 215 000 in July, saw unemployment dip to 5.3%. Monthly hourly-wage indicators have been rising steadily, and the number of weekly jobless claims fell to the lowest level since 1973 in the last week of July. The Bank, however, is less than sanguine. Ms Yellen specifically notes that the low labour force participation rate – at 62.6 %, the lowest in nearly three decades – implies the existence of a shadow pool of unemployment.

Moreover, the second Earnings Cost Index (published on a quarterly basis, and regarded by economists as a more representative indicator of wage growth than hourly earnings data) came in well below expectations. After a buoyant first quarter (0.7%), wage-growth has reverted to a lower trajectory. The Q2 figure of 0.2%, disconcertingly, is also the poorest showing since 1982. The Federated Reserve’s cautious stance regarding growth prospects was also evident in the statements from staff members which were leaked on the 29th of July. Conspiracy theorists and sceptic pundits suggest the leak is an example of the Bank’s more subtle attempts at ‘open-mouth-operations’ prior to engaging in open-market operations. Nonetheless, the consensus view is that the first rate-hike will take place in September 2015.

The simplified rationale behind the Fed’s scrutiny of the labour market: The labour market is indicative of the amount of ‘slack’ in an economy. When the economy is at or near full potential, there is less slack, and more resources (including human capital) are in use. Unemployment declines, wages increase, and prices tend to rise. This anchors inflation expectations and feeds into a virtuous reflationary cycle.

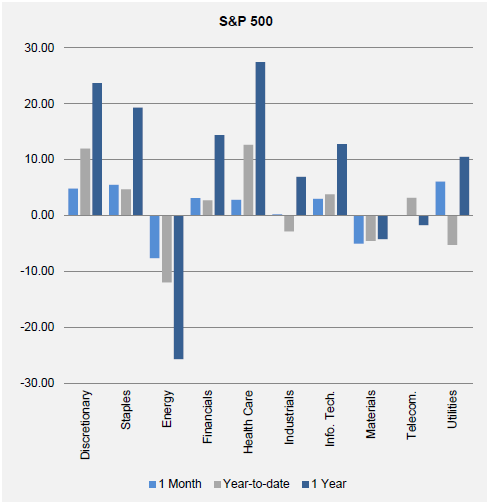

The latest earnings season has surprised to the upside, with roughly 75% of reporting companies (as at 31 July, per Factset) overshooting market expectations. Despite some notable disappointments (Apple in particular), Information Technology – related stocks (Google, Facebook and Twitter) were star performers, with Google reporting a 17% jump in profits. Online retailer Amazon was a similarly welcome surprise, underscoring a cautious return of consumer appetite. Energy-related companies, notably Chevron and Exxon, reported a dismal season, but market participants latched onto the silver lining (having expected 20% more dismal returns). Traditionally defensive sectors (utilities, healthcare and consumer staples) lead sector returns. Consumer discretionaries ticked up nicely, and Healthcare stocks solidified their year-to-date gain, continuing to see significant Merger and Acquisition (M&A) activity. Indeed, Bloomberg reports that July was the 7th most active month for M&A on record, with $430 billion in deals seeing the light. Fairly predictably, against the backdrop of global growth concerns and further commodity dips, Basic Materials and Energy lagged, at -5.02% and -7.65% respectively.

Index sector Returns – USA.

(Source: Eaton Vance)

European markets

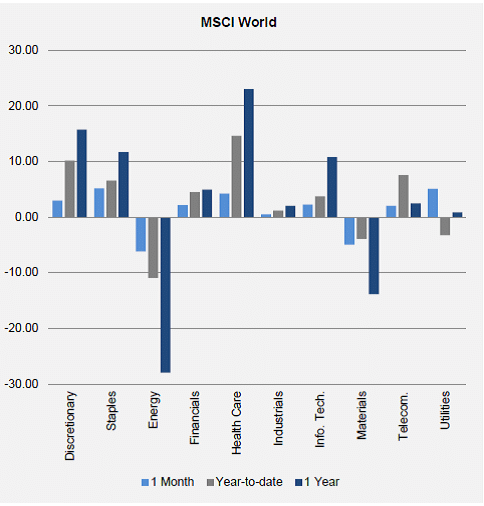

As a last-minute compromise was reached between Greece and its weary creditors, European markets bounced back from a rather volatile June. The MSCI Europe was up by 4%, with Switzerland and Denmark leading their peers at 7% apiece, and Germany’s DAX rising 3%. Country-level statistics are encouraging: traditional laggard France recorded a 6% gain off solid growth and factory-output data; German unemployment is at its lowest level in 34 years, and peripheral market Italy’s PMI rose to its highest level in four years (55.3) and. Overall, the Eurozone remains in expansive territory, with the Markit Composite PMI steady at 52.4. The European Commission’s Economic Sentiment Indicator show that both consumers and corporations stayed upbeat in the face of Greek wobbles. The German Ifo Business Sentiment Survey increased to 108 in July, after three consecutive months of declines, while the European Bank’s lending survey showed a renewed demand for credit. Indicative too of a resurgent Eurozone consumer’s appetite for big-ticket items: new car registrations during July showed a year-on-year increase of 14.6%, the sharpest rise since the onset of the recession. Eurozone unemployment was stable at 11.1%, and preliminary consumer price data points to reflation. Inflation is estimated to be 0.2 % for July, still well below the European Central Bank’s 2% target, fuelling market participants’ optimism that the Bank will extend its asset-purchasing programme. In the aftermath of the Greek debt crisis, safety was still at a premium, and defensive sectors posted the biggest gains. Telecommunications and Consumer Staples recorded 6% gains, while Healthcare was 8% higher. Both the latter sectors were boosted by strong earnings and profit reports; and Vodafone was boosted by sales in its Middle East and Africa operations. As in the US, Materials and energy declined on a slew of poor earnings results and reduced estimates: Energy giant BP reported a $6.3 bn loss, partly attributable to a residual $10 bn charge related to the Gulf of Mexico oil spill; and Glencore lost 19%, with shares falling to the lowest level since their Initial Public Offering (IPO) in 2011.

In line with other developed market peers, the United Kingdom’s FTSE 100 closed in the black, ending July 3% higher. The domestic economic recovery has gained traction, with second quarter growth reported at 0.7%, and the PMI increasing to 51.9. With UK car production at a 7-year high and new vehicle sales figures at record levels in June, it appears British buyers are fairly upbeat, with demand for big-ticket items on the rise. As on the continent, domestically focused sectors, including housebuilders, benefited from strong corporate news-flow. GlaxoSmithKline in healthcare and BAT in consumer staples (cigarettes of course a staple) were notable star performers. The Office for National Statistics indicated that unemployment had ticked up slightly in July to 5.6%, but that average weekly earnings growth had simultaneously increased by 3.2% in the preceding three months. British inflation, however, remains low, and the Bank of England voted unanimously to maintain interest rates at current low and stimulatory levels.

Index sector and Style Returns – Global Average

Asian heavyweights – Japan and China

Japanese markets rallied toward the latter half of the month, the Nikkei registering a 5.46 % gain. Macroeconomic data was somewhat mixed: Manufacturing output increased, with the PMI at 51.4, whilst retail sales grew at a slower rate of 0.9% and household spending unexpectedly declined. Japanese defensive stocks did particularly well, with consumer staples ticking up 9% (Japanese Tobacco again a notable performer. Tokyo Electric reported that profits had tripled from the previous year, and saw its share price surge by 33%, significantly boosting the utilities sector. The majority of Japanese firms are still to report, and analysts are fairly upbeat. The main detractors are likely to be in the technology and electronics industry, with Panasonic and Samsung already undershooting, and Toshiba not yet shrugging of the unease surrounding its accounting-discrepancies. Chinese equities saw another torrid month, with no sectors escaping the panic-selling that marred June month-end. The rise and subsequent collapse of the Chinese stock market witnessed extensive government intervention to prop up equities and the wild see-saw found temporary balance. The lull, however, is precarious, and investors remain jittery as to the longevity of authorities’ support, as well as to the unintended consequences of monetary policy-stimulus measures. The news-flow from China, at any event, has not engendered confidence. The Caixin-Markit Purchasing Managers’ Index slumped to 48.2 in July, the lowest level in 15 months. Anecdotal evidence on the demand for electricity suggests that production has declined by an even greater margin. In the first half of the year, the financial sector contributed roughly 30% to GDP growth (versus an average of 10% in previous years). This effect is set to drop out in subsequent quarters, as a consequence of tighter regulations and the decline in equities. Official growth statistics nonetheless indicate that the Chinese economy expanded at 7% for the second quarter.

Monetary policy can be a blunt tool. Aggressive easing by the People’s Bank of China led to a sharp increase in margin trading, fuelling the dizzy heights the stock market attained. Investors were rushing to a market buoyed by easy credit and institutional inflows on the new Shanghai-Hong Kong Stock Connect. At the first signs of a clampdown on margin trading, within two weeks margin calls had wiped out nearly 70% of the previous 3 months gains. Furthermore, while the fresh liquidity flooding the market is no longer being channelled to margin lending, other speculative ventures are still relatively unregulated (eg property). New asset class bubbles could easily arise. The continued intervention of the POBC has critically called into question whether the Communist government is credibly committed to market liberalization. Ultimately, a lack of credibility would do more harm than good to the country’s long-run growth prospects. Notable symptoms of global scepticism: Chinese A-shares were rejected for inclusion in the widely used MSCI Emerging Markets Index. And the IMF rejected the Yuan for Special Drawing Rights status (SDR currencies – the Yen, the Dollar, Sterling and the Euro – form a special reserve asset for the Fund).

Emerging Markets

Emerging markets significantly underperformed their developed peers, weighed down by looming Fed lift-off, declining commodity prices and developments in emerging giants China, Brazil and Russia. Emerging Asian minnows were largely swallowed by the Chinese plunge, and the region lagged its European, Middle-Eastern and African peers. The Philippines, Thailand and Indonesia all declined, despite little change in domestic fundamentals. South Korean stocks lost 2%, as an outbreak of MERS, and poor results from tech-giant Samsung dragged on the bourse. India was a once again the regional darling, rising by 2%. Authorities reported GDP growth of 7.3% for the second quarter, and structural reforms are gaining momentum. India is noted for its ease of doing business (ranking fourth globally in terms of number of start-up businesses) and competitive valuations make Indian markets particularly attractive to cautiously-risky offshore investors. Latin American markets were similarly led lower by regional powerhouse Brazil. The continued commodity-price slump has done little to boost the country’s long-term growth prospects, and domestic policies appear ineffectual in curtailing domestic inflation and unemployment. Standard and Poors downgraded Brazil’s sovereign debt outlook from stable to negative during July and other ratings agencies may follow suit. The Brazilian market declines were amplified by the sharp depreciation of the currency against the USD. Within Emerging Europe, Hungarian stocks were the outlying performer, registering a gain of just under 1%. The Russian bourse lagged, with economic growth still in the doldrums. The rouble declined by 9% against the USD, and inflation is rampant at over 15%, despite the 6% cumulative rate cut by the Central Bank for the year to date. Domestic woes have been exacerbated by renewed geopolitical tension with Ukraine and Eurozone trade-partners (July saw a crucial gas-pipeline to Ukraine being cut off, as well as the burning of banned imported foodstuffs from the EU). Turkish assets slipped, and the Lira declined, amidst political uncertainty and social unrest. African economies lost ground, with Kenya and Nigeria amongst the worst performers in USD terms. The Nigerian economy continues to be hard-hit by declines in oil-and-gas earnings, reporting that external trade had declined by 17.1% in the First Quarter. The Nigerian exchange ended -9.03% lower. Kenya ended -10.72% in the red, as financials recorded large losses toward month-end. The Zambian mining sector saw hydro-electricity shortages compound large losses sustained due to declining copper prices. Despite continued tension (geopolitical and terrorism-related) in near neighbours Egypt and Tunisia, the Moroccan market bucked the overall trend, ending 1.51% higher. On an encouraging note as to the growth prospects of a number of African countries: Statfor, a geopolitical intelligence agency, has flagged Kenya, Tanzania, Ethiopia and Uganda as potentially becoming mini-Chinas, as manufacturing shifts away from the Asian giant.

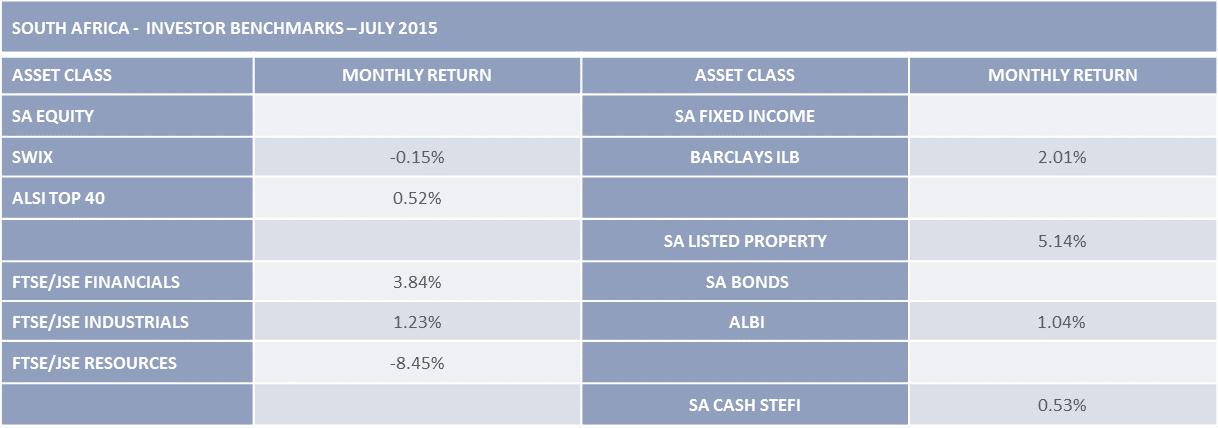

South Africa

As global investors rotated toward developed markets, and commodity prices declined further, South African companies faced a difficult July. Despite constrained domestic conditions, however, SA equities witnessed net foreign purchases of R5.3 billion, whilst R4.3 billion flowed to SA bonds. Data on the employment front was somewhat more upbeat than in the preceding quarter: Unemployment contracted to 25%, from 26.4%, and 198 000 new jobs were added, albeit mostly in the informal sector (177 000 versus 39 000 in formal sector employment, and losses in agriculture). The balance of trade was favourable, as the surplus widened to R5.8 bn. Domestic demand, however, remains subdued: a telling statistic (especially in contrast to developed peers), total vehicle sales declined by 6.1% year on year, and consumers feel unable to accommodate big-ticket items in their constrained budgets. Perceived job insecurity is likely to weigh on consumer as well. As commodity prices remain at lower levels, restructuring and scaling back of human resources and capital expenditure has already been evident in the local mining and manufacturing sectors. Gold miners, nonetheless, are presently testing their bargaining power. CPI data came in below expectations (at 4.7%). Nonetheless, the South African Reserve Bank cited the upside risk to the inflation outlook (including Rand vulnerability, and wage increases which outstrip inflation and productivity growth). The committee therefore elected to raise the repo rate by 25 bps. The Rand responded by dropping to multi-year lows against the dollar. Aided by the currency’s vulnerability, Rand hedges were highly in demand on the JSE. In contrast to developed peers, local large caps outperformed small and mid-caps. In sector terms, financials notably outstripped person positive company updates. Resources predictably plunged. Listed property, after a mid-year wobble, resumed its upward trend, and remains the best-performing asset class for the year to date.

Currencies, Commodities and Fixed Income

The Greenback continued to strengthen throughout July, while commodity-based currencies (eg the Australian dollar and Norwegian Krone) and emerging markets depreciated notably. The Rand slipped 4.1% against the dollar; 3.1% against the British Pound; 2.4% against the Yen; and 1.9% against the Euro. Other emerging market currencies, the Lira, Real and Chilean Peso, all fared relatively worse.

Commodities slumped, on a lack of demand from China, the global oil-supply glut and the stronger USD. Chinese demand continues to dominate market expectations (constituting 15% of demand for oil, 31% of demand for copper, and 60% of demand for iron ore). Copper has consequently fallen to a fresh six-year low. The Gold Mining Index has declined to an all-time low, as gold priced tumbled during July. With no sign that the global glut will be either mopped up, or production curtailed, Brent Oil resumed its slide. More tellingly, crude oil futures settled at their lowest levels since March, demonstrating analysts’ expectations for further declines (potentially $45 per barrel before the end of the year).

Within the fixed income space, as global growth fears resurfaced, developed market sovereign bonds were back in demand. US Treasuries advanced and the yield on 10-year T-bills declined from 2.35 to 2.18%. Fellow safe-haven sovereigns saw similar declines: German Bund yields ended at 0.64% and UK Gilts at 1.88%. Italian and Spanish Treasuries’ yields had more pronounced dips (56 and 46 bps respectively), with appetite for peripherals returning as the Grexit was averted. Overall, developed market yield curves flattened: With US hikes imminent, longer-dated bonds remain less sensitive to interest rate changes, and are still in favour with institutional investors who need to match long-run liabilities. Investment grade corporate bonds outperformed high-yield bonds, with UK corporates outperforming US and Eurozone counterparts. Emerging market bonds saw net outflows, as sentiment was notably risk-off. There were pockets of stability, however, with Mexican sovereigns proving resilient. EM corporates, though outperforming EM sovereigns, fared poorly against developed counterparts, weighed down by Brazilian bonds (as further arrests from the Petrobras scandal ensued).

Conclusion

Investors may be able to take a brief breather during August – with Eurozone stability restored, earnings season largely concluded, and the Fed unlikely to significantly alter (or further clarify) its guidance. Unless the slumbering Chinese manufacturing giant resurfaces, and the dollar reverse its year-to-date rise, the outlook for commodities remains weak. Toward month-end, however, global nerves are sure to be evident, particularly within emerging markets, as lift-off looms.