Global Market Commentary: May 2026

AI momentum and earnings strength extend global market rally

Global markets extended their recovery in May as AI-related investment, strong corporate earnings and improved geopolitical sentiment supported risk appetite. Developed markets were led by the US and Japan, while emerging markets benefited from North Asian technology supply-chain strength. Inflation remained a key policy constraint, with central banks balancing sticky price pressures against signs of uneven growth. In commodities, easing oil-related tensions helped reduce energy pressure, while precious metals corrected and the dollar firmed modestly. Bond markets remained sensitive to shifts in inflation expectations, geopolitical developments and changing assumptions about the timing of future rate cuts.

Key highlights:

- AI-related investment and strong earnings continued to support global risk appetite.

- Emerging markets outperformed as North Asian technology supply chains benefited from sustained AI demand.

- Inflation and central bank policy remained key drivers of market expectations across major economies.

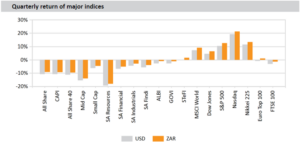

Global equity markets extended April’s gains in May, with the MSCI World returning 4.6% (USD) and the MSCI Emerging Markets Index outperforming with 9.7% (USD). Markets were driven by three key themes: the artificial-intelligence capital-expenditure supercycle, an exceptionally strong first-quarter earnings season, and growing optimism around a possible US-Iran deal that could ease the oil shock. US and Japanese equities led developed markets to record levels. Bond markets were more volatile than equities, as yields reacted quickly to shifts in the geopolitical narrative.

The US economy expanded at an annualised 1.6% in the first quarter, revised down from the 2.0% advance estimate, but higher than the 0.5% recorded in the fourth quarter. Headline inflation accelerated to 3.8% year-on-year in April, the fastest pace since May 2023, up from 3.3% in March, as energy costs rose 17.9%. Core inflation increased to 2.8% from 2.6%, while the unemployment rate held at 4.3%. The Federal Reserve did not hold a policy meeting in May, and with inflation re-accelerating, markets pushed expectations for the next rate cut into late 2026 or 2027. US equities advanced to record highs, with the S&P 500 up 5.3% (USD), the Nasdaq Composite up 8.4% (USD) and the Dow Jones up 2.8% (USD). The first-quarter earnings season was exceptionally strong, with about 83% of S&P 500 companies beating estimates and earnings growing roughly 30% year-on-year. NVIDIA was the primary catalyst as hyperscaler capital expenditure ran at about $725 billion for 2026.

European equities advanced but lagged the US and Japan, with the Euro Stoxx 50 up 2.9% (EUR) and the broader market up 3.1% (EUR). Euro-area inflation rose to 3.0% in April from 2.6% in March, the highest level since September 2023, driven by a 10.8% increase in energy prices, while core inflation eased to 2.2% from 2.3%. A European Central Bank rate hike in June looks likely to anchor inflation expectations. The composite PMI fell to its lowest level since late 2023, pointing to sluggish growth.

UK inflation eased to 2.8% in April from 3.3%, the lowest reading since March last year, helped by an energy price cap and softer housing services inflation. The Bank of England maintained a restrictive stance amid sticky services inflation. The FTSE 100 rose 0.7% (GBP) during a volatile month. UK manufacturing slipped into a slight contraction, although gilts outperformed the global government bond market as yields fell late in the month.

Japan’s Nikkei 225 gained 11.9% (JPY), the strongest performance among major global indices, surpassing the 66 000 level for the first time, while the broader market rose 6.2% (JPY). First-quarter GDP beat expectations at 2.1% quarter-on-quarter, led by consumption. Headline inflation edged down to 1.4% in April from 1.5%, with core inflation also at 1.4%, remaining below the Bank of Japan’s 2% target for a third consecutive month. The Bank of Japan has shown greater tolerance for higher headline inflation.

China’s CSI 300 rose 1.9% (CNY), led by A-shares, while the MSCI China Index declined 3.0% (USD) as investors took profit in technology and semiconductor shares. The official manufacturing PMI slipped to the neutral 50 mark from 50.3, while the non-manufacturing PMI improved to 50.1. Inflation rose to 1.2% year-on-year in April from 1.0%, driven by higher energy and transport costs despite falling food prices. The People’s Bank of China continued to ease policy, although property weakness and cautious household spending limited the recovery.

Emerging markets outperformed all other asset classes, with the MSCI Emerging Markets index returning 9.7% (USD). The gains were led by strong returns from South Korea, up about 33%, and Taiwan, up about 14%, as both benefited from their positioning in the AI supply chain and hyperscaler-led investment demand. India’s SENSEX fell 2.6% (INR) and Brazil’s Bovespa declined 7.2% (BRL).

Brent crude had another volatile month, falling 17.5% to end near $91.12 per barrel as peace hopes eased the oil shock, after trading above $110 for much of May. Outside oil, commodity performance was mixed. Gold declined 1.7% to $4 540.26 and platinum fell 3.4% to $1 920.19, while palladium dropped 11.3% to $1 360.64 as precious metals corrected. Silver gained 2.1% to $75.30 and copper rose 5.3% to $13 599.71. Iron ore slipped 1.5% to $105.37, while coal advanced 3.3% to $116.75.

The US dollar Index rose modestly by 0.3%, supported by relatively higher US yields and safe-haven demand. The rand strengthened 3.0% against the US dollar to close at R16.20, helped by the domestic rate hike, softer US economic data and a weaker dollar. The rand has now strengthened roughly 2.3% against the dollar for the year to date.

World Market Indices Performance

About RisCura Global monthly market commentary

Explore the retrospective RisCura Global monthly Commentary, spanning vital regions like the USA, UK, Europe, and emerging markets. Gain clarity on economic phenomena with benchmarks on inflation, interest rates, commodity prices, and credit ratings. Tailored for value-driven investors, our insights inform asset allocation across diverse global markets.

Stay informed – subscribe now for insightful perspectives from the RisCura Global Commentary.