Global Market Commentary: March 2026

Markets reprice as energy shock drives risk-off sentiment

Global markets moved into a broad risk-off phase in March as geopolitical tensions, higher energy prices and rising yields weighed on sentiment across regions and asset classes. Developed markets came under pressure as softer growth momentum, persistent inflation and tighter financial conditions reduced support for both equities and bonds. Emerging markets were further challenged by external shocks and ongoing domestic adjustment, with China remaining under strain. Commodities and currencies played a central role in the month’s repricing, as the energy shock lifted inflation concerns, supported the US dollar and added pressure to emerging market currencies. Market volatility increased meaningfully through the period.

Key highlights:

- Global markets shifted into a broad risk-off phase in March.

- Higher energy prices and rising yields drove cross-asset repricing.

- Emerging markets remained under pressure as the US dollar strengthened.

Global financial markets experienced a broadbased selloff during March as geopolitical developments, elevated energy prices and rising risk aversion drove a sharp repricing across equities, bonds and currencies. The MSCI World Index declined 6.4% (USD), reflecting weakness across most major developed markets, while the MSCI Emerging Markets Index fell 13.1% (USD), marking a significant divergence between developed and emerging market performance. Equity market volatility increased meaningfully over the month as investors responded to heightened uncertainty around global growth, inflation trajectories and supplyside risks stemming from energy markets. Bond markets also weakened as yields rose in response to higher energy prices and inflation concerns, limiting the traditional defensive role of fixed income assets. Global growth indicators softened, with survey data pointing to slowing momentum across several regions and reinforcing the riskoff tone that characterised March.

In the United States, macroeconomic data painted a picture of slowing momentum against a still-resilient inflation backdrop, while markets repriced rate expectations and risk premia. Real activity indicators weakened following the downward revision to US growth, with Q4 2025 GDP revised to an annualised 0.7%, materially below the earlier 1.4% estimate. Inflation remained sticky though not accelerating, with February headline CPI steady at 2.4% year-on-year and core CPI at 2.5% year-on-year, alongside a 0.3% month-on-month increase in headline CPI. Labour market conditions softened at the margin, as the unemployment rate rose to 4.4% in February and non-farm payrolls declined by 92,000. Equity performance was weak, with the S&P 500 falling 5.0% (USD), and the Nasdaq Composite declining 4.7% over the month. Bond markets reflected tighter financial conditions, with the US 10-year yield rising towards 4.38%, consistent with expectations that the policy stance could remain restrictive for longer in the presence of energy-driven inflation risk.

Europe and the UK faced a particularly acute transmission of the energy shock into inflation and confidence, against a backdrop of already modest growth. Euro area inflation rose to 2.5% year-on-year in March from 1.90% in February, driven by an acceleration in energy inflation to 4.9%, while core inflation eased to 2.3% year-on-year. Survey indicators signalled near-stagnation, with the euro area flash composite PMI falling to 50.5 in March. Monetary policy remained on hold in the euro area, with the European Central Bank keeping the main refinancing rate at 2.15%, the deposit facility at 2.00%, and the marginal lending rate at 2.40%, while highlighting heightened uncertainty linked to the conflict. European equities moved lower in line with global risk assets, with the STOXX All Europe Index down 7.6% (EUR) for the month. In the UK, inflation remained elevated, with February CPI at 3.0% year-on-year and core inflation at 3.2% year-on-year, while the Bank of England held the Bank Rate at 3.75% on a unanimous 9-0 vote in favour of no change. UK rates repriced higher, with 10-year gilt yields ending just below 5.00%, and equity markets reflected the risk-off tone, with the FTSE 100 down 6.2% (GBP).

Japan was not insulated from the global repricing, as risk aversion and energy-market dynamics weighed on equities and financial conditions even as domestic inflation momentum eased. Japan’s headline inflation eased for a fourth consecutive month in February, supported by stabilising food prices and subsidies, although higher energy costs began to re-emerge as a pressure point. Equity markets reflected the global drawdown, with the Nikkei 225 falling 12.6% (JPY), placing Japan among the weaker major markets in March’s risk-off move. The policy backdrop remained shaped by a cautious Bank of Japan stance in the face of trade, energy and currency-related risks, while market commentary also pointed to higher domestic yields and a weaker currency against the US dollar.

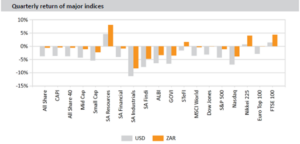

China and broader emerging markets faced a challenging combination of external energy shocks and ongoing domestic adjustments, contributing to significant underperformance relative to developed markets. China’s inflation print firmed, with CPI rising to 1.3% year-on-year in February and core inflation at 1.8% year-on-year, partly reflecting Lunar New Year effects and a rebound in food prices. Chinese equities declined amid heightened volatility, with MSCI China down 7.7% (USD) and the CSI 300 down 5.5% (CNY). Broader emerging markets sold off sharply, with the MSCI Emerging Markets down 13.1% (USD), consistent with the month’s global risk-off tone and the impact of higher energy costs on import-dependent economies. Among key emerging markets, Brazil was comparatively resilient, with the BVSPA down 0.7% (BRL), while India saw a larger decline with the SENSEX down 11.5% (INR).

Commodities and currencies were central to March’s cross-asset repricing, with energy markets driving a broad reassessment of inflation trajectories and risk premia, while precious metals reversed from prior strength. Oil rose 42.7% (USD) over the month, ending at $103.97, reflecting heightened concern over supply and transport disruption risks. Precious metals declined sharply despite elevated uncertainty, with gold falling 11.6% (USD) to $4,668.06 and silver falling 19.9% (USD) to $75.17. Platinum and palladium also weakened, with platinum down 17.5% (USD) to $1,953.65 and palladium down 17.2% (USD) to $1,480.41. Industrial commodities were mixed, with copper falling 7.8% (USD) to $12,256.76 while iron ore rose 7.2% (USD) to $105.48 and coal rose 12.0% (USD) to $110.40.

Currency moves reflected the month’s risk aversion and energy-driven dollar strength, with the rand weakening 7.5% against the US dollar to end the month at R17.12 per USD.

World Market Indices Performance

About RisCura Global monthly market commentary

Explore the retrospective RisCura Global monthly Commentary, spanning vital regions like the USA, UK, Europe, and emerging markets. Gain clarity on economic phenomena with benchmarks on inflation, interest rates, commodity prices, and credit ratings. Tailored for value-driven investors, our insights inform asset allocation across diverse global markets.

Stay informed – subscribe now for insightful perspectives from the RisCura Global Commentary.