Global Market Commentary: April 2026

Risk appetite returns as trade tensions ease

Global equity markets rebounded sharply in April 2026, recovering from the prior month’s trade-driven weakness as US trade policy rhetoric eased and risk appetite improved. Developed markets advanced, with US equities reaching all-time highs on a strong first-quarter earnings season, while European and UK markets gained despite subdued domestic conditions. Emerging markets outperformed, supported by US dollar weakness and renewed demand for higher-risk assets, with North Asian markets leading gains. Central banks largely held rates steady, although inflation pressures remained visible across major economies. Commodity performance was mixed, as energy prices rose on Middle East supply concerns while precious metals retreated.

Key highlights:

- Global equities recovered as trade tensions eased and risk appetite improved.

- Emerging markets outperformed, supported by US dollar weakness and strong North Asian market gains.

- Commodities were mixed, with energy prices rising while precious metals retreated from elevated levels.

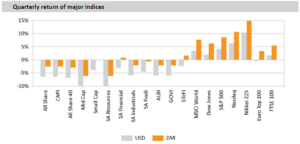

Global equity markets rallied sharply in April 2026, recovering materially from the trade-driven weakness of the prior month. The MSCI World Index gained 9.6% (USD), while the MSCI Emerging Markets Index outperformed significantly, advancing 14.7% (USD). The improvement in risk sentiment was supported by a de-escalation in US trade policy rhetoric, a resilient US corporate earnings season, and continued monetary policy support across key central banks. Emerging market equities benefited disproportionately from US dollar weakness and renewed investor appetite for higher-risk assets, with North Asian markets, particularly South Korea and Taiwan, delivering exceptional gains. Commodity markets were mixed, with energy prices supported by Middle East supply concerns, while precious metals retreated from elevated levels.

The US economy posted preliminary first-quarter 2026 GDP growth of 2.0% annualised, below the consensus expectation of 2.3% but a marked improvement from the prior quarter’s contraction. Consumer spending growth moderated to 1.6% annualised, while business equipment investment rose strongly at 10.4% annualised. Headline consumer price inflation rose to 3.3% year-on-year in March, up from 2.4% in the prior month, driven largely by energy prices which advanced 12.5% year-on-year. Core CPI edged higher to 2.6% year-on-year. The labour market remained resilient, with non-farm payrolls increasing by 178 000 jobs in March and the unemployment rate declining slightly to 4.3%. The Federal Reserve held the federal funds rate unchanged at 3.50%-3.75% at its April meeting., The decision was carried by an 8-4 vote, the highest number of dissents since October 1992, reflecting growing internal debate over the appropriate pace of further easing.

US equity markets surged, with the S&P 500 rising 10.5% (USD) and the Dow Jones Industrial Average gaining 7.1% (USD). The S&P 500 reached all-time highs, supported by a strong first-quarter earnings season in which approximately 84% of companies beat earnings estimates and aggregate S&P 500 earnings per share grew an estimated 14.5% year-on-year.

European equity markets advanced in April, supported by improved global risk sentiment and a weaker US dollar, even as domestic economic conditions remained subdued. The STOXX Europe 600 gained, with European ex-UK equities rising 5.7% in local currency terms. The European Central Bank held its main refinancing rate at 2.15% and the deposit facility rate at 2.00% at its April meeting, with the decision unanimous. Euro area headline inflation rose to 3.0% year-on-year in April on a preliminary basis, up from 2.6% in March, driven in part by energy prices which rose 10.9% year-on-year. Eurozone PMI data pointed to contraction in overall business activity, highlighting ongoing structural headwinds to growth.

In the United Kingdom, the Bank of England held its base rate at 3.75%, with the Monetary Policy Committee voting 8-1 to hold. The single dissent was in favour of an increase to 4.0%. UK headline consumer price inflation rose to 3.3% year-on-year in March, up from 3.0%, driven by transport and energy costs. Services activity expanded modestly, while manufacturing remained under pressure. The FTSE 100 gained 2.3% (GBP) over the month.

Japanese equities delivered strong outperformance in April, with the Nikkei 225 advancing 16.1% (JPY), supported by improved global trade sentiment and a rotation into export-oriented markets. The Tokyo Stock Price Index (Topix) gained 6.6% (JPY). The Bank of Japan held its policy rate at 0.75% at its April meeting, with the vote split 6-3. The three dissenting members, Hajime Takata, Naoki Tamura, and Junko Nakagawa, all preferred an immediate increase to 1.00%, signalling growing hawkish momentum within the committee. The Bank of Japan revised its fiscal year 2026 core consumer price inflation forecast upward to 2.8% from 1.9% previously, while trimming its fiscal year 2026 GDP growth forecast to 0.5% from 1.0%, reflecting trade uncertainty. Japan’s flash manufacturing PMI for April printed at 54.9, its fastest rate of expansion in four years. Headline consumer price inflation rose to 1.5% year-on-year in March from 1.3%, with transport costs rising at their fastest pace in four months. Core inflation, excluding food and energy, stood at 1.8% year-on-year, marginally below the Bank of Japan’s 2.0% target.

Chinese equity markets advanced in April, with the CSI 300 Index gaining 8.2% (CNY) and the MSCI China Index rising 3.6% (USD), supported by domestic policy measures and improving manufacturing activity. China’s official manufacturing PMI for April rose to 50.3, its strongest reading since 2020, pointing to a broadening recovery in industrial output. Consumer price inflation eased to 1.0% year-on-year in March from 1.3%, reflecting subdued domestic demand and the effect of fuel price controls, while core inflation held at 1.1% year-on-year. The People’s Bank of China maintained its one-year and five-year loan prime rates at 3.0% and 3.5% respectively.

Elsewhere within emerging markets, the MSCI Emerging Markets Index’s exceptional performance was driven disproportionately by North Asian markets. South Korea surged 38.2% (USD) and Taiwan advanced 26.2% (USD), as global technology and semiconductor equities experienced a strong re-rating. India’s Sensex rose 6.9% (INR), recovering from recent weakness, while Brazil’s Bovespa was broadly flat, declining 0.1% (BRL).

Commodity markets delivered a mixed performance in April. Brent crude oil rose 6.2% over the month, closing at $110.40 per barrel, supported by heightened geopolitical risk in the Middle East, which disrupted shipping through the Strait of Hormuz and tightened supply expectations. Brent reached an intraday high of approximately $126 per barrel during the month. Gold declined 1.1% (USD) to close at $4 617.85 per troy ounce, retreating marginally from exceptional levels as some safe-haven demand unwound in line with improved risk sentiment. Silver fell 1.9% (USD) to $73.75 per troy ounce. Copper advanced 5.3% (USD) to $12 910.76 per metric tonne, reflecting improving global industrial activity signals. Platinum rose 1.8% (USD) to $1 987.75 per troy ounce and palladium gained 3.6% (USD) to $1 533.07 per troy ounce. Iron ore advanced 1.5% (USD) to $107.02 per metric tonne, while coal gained 2.4% (USD) to $113.00 per metric tonne. The US dollar weakened broadly during the month, with the DXY Index declining as risk appetite improved.

The South African rand strengthened 2.4% against the US dollar, closing at $16.70 per US dollar, supported by improved emerging market sentiment, firmer commodity prices, and broad US dollar weakness.

World Market Indices Performance

About RisCura Global monthly market commentary

Explore the retrospective RisCura Global monthly Commentary, spanning vital regions like the USA, UK, Europe, and emerging markets. Gain clarity on economic phenomena with benchmarks on inflation, interest rates, commodity prices, and credit ratings. Tailored for value-driven investors, our insights inform asset allocation across diverse global markets.

Stay informed – subscribe now for insightful perspectives from the RisCura Global Commentary.