Middle East escalation – what investors should monitor

Recent military exchanges between the United States, Israel and Iran have escalated tensions across the Middle East and widened the geographic scope of the confrontation. The speed of retaliation and the spread of strikes across multiple regional actors has increased uncertainty around how contained the situation will remain.

For investors, the key question is not only the geopolitical development itself, but how it transmits into global markets. Historically, geopolitical shocks affect asset prices primarily through a small number of macro channels – most importantly energy markets, inflation expectations and risk premia.

The situation remains fluid. But understanding these transmission mechanisms helps frame what matters for markets and what signals would change the outlook.

Why this matters for markets

Energy – the primary transmission channel

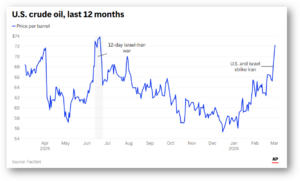

Energy markets are typically the most direct channel through which Middle East tensions affect global financial conditions.

The region sits at the centre of several critical energy routes, including the Strait of Hormuz, through which roughly one fifth of global petroleum flows transit. Even perceived disruption risks can therefore translate quickly into higher oil prices.

This dynamic has already been visible in market reactions following the latest escalation, with oil prices rising as investors reassessed risks to supply routes and regional stability.

Importantly, markets often respond not only to realised disruptions but to probabilities of disruption. Energy therefore becomes the first channel through which geopolitical risk is reflected in global asset pricing and portfolio construction.

Inflation and rates – the macro spillover

Energy prices are closely linked to inflation expectations and, therefore, to the outlook for interest rates.

Higher oil prices feed directly into headline inflation and can tighten financial conditions even before central banks respond. In recent market movements, US Treasury yields edged higher as investors reassessed the inflation implications of the escalation and the potential limits on the pace of monetary easing.

Geopolitical shocks often produce a temporary flight to safety in bonds. But if the shock pushes energy prices higher, that effect can quickly reverse as inflation concerns re-emerge.

For investors, this interaction between energy prices and inflation expectations is a key macro channel to monitor.

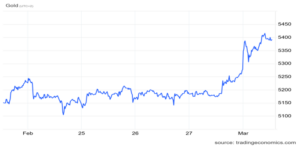

Risk premia – how markets typically respond

Beyond the direct macro effects, geopolitical shocks also influence markets through changes in risk premia.

Periods of elevated geopolitical uncertainty typically see investors rotate toward defensive assets such as gold and the US dollar, both of which tend to benefit from safe haven flows during periods of global stress.

At the same time, risk assets may incorporate higher geopolitical risk premia as investors reassess uncertainty around growth, supply chains and regional stability.

These adjustments do not necessarily imply a structural shift in the global macro environment. In many cases, markets treat such events as tactical risk shocks unless they translate into sustained economic disruption.

What we are watching

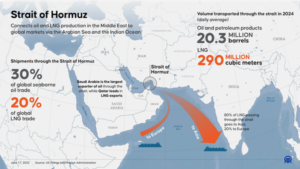

The Strait of Hormuz

One of the most important potential escalation points remains the Strait of Hormuz.

The waterway is one of the world’s most critical energy chokepoints, carrying around 20% of global petroleum consumption and a significant share of LNG trade. Disruption – or even the credible threat of disruption – could transmit rapidly into global energy markets and inflation expectations.

Because alternative routes are limited, developments affecting shipping flows or security in this corridor would likely have outsized market implications.

Signals that would change the outlook

At present, market behaviour remains broadly consistent with a geopolitical risk event rather than a structural macro regime shift.

From an investment perspective, the key variables to monitor include:

- Evidence of sustained disruption to energy supply or shipping flows

- Escalation that widens the conflict to additional regional actors

- Persistent upward pressure on energy prices feeding into inflation expectations

- Shifts in central bank communication in response to energy-driven inflation risks

A scenario in which energy supply routes are materially disrupted would alter the macro-outlook. Current evidence, however, suggests markets are primarily pricing elevated risk premia rather than sustained supply constraints.

In that environment, the appropriate response is heightened monitoring rather than immediate portfolio repositioning.

Subscribe for future investment insights and commentary:

https://riscura.com/subscribe/