Global Market Commentary: June 2026

Technology pressure and commodity reversal shape June markets

Global markets pulled back in June after May’s rally, as easing Middle East tensions reversed the oil shock and triggered a broad decline across commodities. Technology shares also came under pressure as an artificial-intelligence and semiconductor sell-off weighed on sentiment, although markets stabilised later in the month as geopolitical concerns eased and mega-cap technology shares recovered. The US market was mixed, Europe advanced, Japan remained a standout performer, and China’s performance diverged across mainland and Hong Kong-listed equities. Emerging markets lagged in dollar terms, while a firmer US dollar and weaker commodity prices pressured resource-linked assets and currencies.

Key highlights:

- Global sentiment softened as technology weakness and shifting geopolitical risk weighed on markets.

- Japan remained resilient, supported by technology strength, fiscal stimulus and corporate reform.

- Commodity markets declined as geopolitical risk premiums unwound and energy pressure eased.

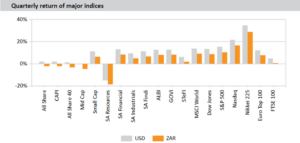

Global equity markets entered June at record highs but pulled back over the month, with the MSCI World returning -0.7% (USD) and the MSCI Emerging Markets index returning -1.4% (USD). Three themes drove markets: a Middle East ceasefire that unwound the oil shock and sent commodities tumbling, an artificial-intelligence and semiconductor sell-off concentrated in technology shares, and uncertainty around the change in US Federal Reserve leadership. Sentiment improved later in the month as US-Iran tensions eased, and mega-cap technology shares recovered. Japan and the Dow Jones reached record highs, while bond and commodity markets remained volatile.

The US economy expanded at an annualised 2.1% in the first quarter, revised up from 1.6% and well above 0.5% in the prior quarter, as investment and government spending recovered. Headline inflation accelerated for a third consecutive month to 4.2% year-on-year in May from 3.8% in April, the highest since April 2023, as energy costs jumped 23.5%. Core inflation edged up to 2.9% from 2.8%, while the unemployment rate held at 4.3%. At its June meeting, the first chaired by Kevin Warsh, the Federal Reserve held the federal funds rate at 3.50% to 3.75% in a unanimous vote, though updated projections showed nine officials expected a rate hike by year-end. US equities were mixed as a rotation out of technology gathered pace, with the Nasdaq down 2.8% (USD) and the S&P 500 easing 1.0% (USD), while the Dow Jones gained 2.5% (USD) to a record high. Despite the pullback, the S&P 500 posted its strongest first half since 2021.

European equities advanced, with the STOXX All Europe index up 2.3% (EUR), as the region’s lighter technology exposure cushioned it from the global sell-off. Euro-area inflation rose to 3.2% year-on-year in May from 3.0%, the highest since September 2023, driven by a 10.9% increase in energy prices, while core inflation climbed to 2.6% from 2.2%. The European Central Bank raised its three key rates by 25 basis points, taking the deposit rate to 2.25%, citing inflation pressures from the Middle East conflict. It also raised its inflation forecasts, now seeing headline inflation averaging 3.0% in 2026, 2.3% in 2027 and 2.0% in 2028, before returning to target, and trimmed its 2026 growth outlook to 0.8%.

UK inflation held at 2.8% year-on-year in May, unchanged from April and down from 3.3% in March, the lowest level since early last year, as slowing food prices offset rising transport costs. The Bank of England kept its Bank Rate at 3.75% in a 7-2 vote, with two members preferring a 25-basis point hike to guard against second-round effects. The FTSE 100 advanced 1.0% (GBP) in a volatile month. First-quarter GDP rose 0.6%, though underlying momentum remained subdued.

Japan’s Nikkei 225 climbed 5.7% (JPY) to repeated record highs, again making it the standout major market. The index was supported by strength in artificial-intelligence and semiconductor shares, fiscal stimulus and corporate reform. Headline inflation edged up to 1.5% in May from 1.4%, while core inflation held at 1.4%, remaining below the Bank of Japan’s 2% target for a fourth consecutive month. The Bank of Japan raised its policy rate to 1%, the highest level since 1995, as inflation and yen concerns took hold.

China’s CSI 300 rose 2.3% (CNY) and the Shanghai Composite gained 0.6% (CNY), but the MSCI China index fell 7.1% (USD) as the technology sell-off hit Hong Kong, where the Hang Seng dropped 9.1% (HKD). The official manufacturing PMI edged up to 50.3 from 50.0, remaining above the level that separates expansion from contraction, while the non-manufacturing PMI rose to 50.2. Inflation held at 1.2% year-on-year in May, with food prices falling 1.7%, while transport costs rose. The People’s Bank of China kept policy accommodative to support the recovery.

Emerging markets lagged in US dollar terms, with the MSCI Emerging Markets index returning -1.4% (USD) as a firmer dollar eroded returns. In local-currency terms, performance was more mixed, with India’s SENSEX up 2.6% (INR) and Brazil’s Bovespa down 1.0% (BRL). The technology and semiconductor sell-off weighed on Asian markets, even as several bourses posted local-currency gains.

Brent crude tumbled 19.9% to end near $72.95 per barrel as a US-Iran ceasefire eased the four-month oil shock and tankers resumed transit through the Strait of Hormuz. Precious metals sold off sharply as geopolitical risk premiums unwound, with gold down 11.7% to $4 008.02, platinum down 19.2% to $1 552.52, silver down 22.2% to $58.60 and palladium down 10.9% to $1 212.14. Copper eased 1.8% to $13 348.90 and iron ore fell 6.0% to $99.04, while coal declined 7.9% to $107.50.

The US dollar firmed over the month on safe-haven demand and relatively higher yields. The rand weakened 1.2% against the dollar to close at R16.39 per US dollar, pressured by lower precious metals prices and broad dollar strength. Against a softer pound and euro, the rand strengthened 0.5% and 1.1% respectively. The rand has firmed roughly 1.1% against the dollar for the year to date.

World Market Indices Performance

About RisCura Global monthly market commentary

Explore the retrospective RisCura Global monthly Commentary, spanning vital regions like the USA, UK, Europe, and emerging markets. Gain clarity on economic phenomena with benchmarks on inflation, interest rates, commodity prices, and credit ratings. Tailored for value-driven investors, our insights inform asset allocation across diverse global markets.

Stay informed – subscribe now for insightful perspectives from the RisCura Global Commentary.