Global Market Commentary: February 2026

Rotation reshapes markets as EM leads and commodities firm

Global risk assets delivered another broadly constructive February, but with clear dispersion across regions and styles. Investors rotated away from US mega-cap technology into value and more cyclically exposed sectors, while emerging markets outperformed on the back of AI-related infrastructure themes and commodity exporters. Geopolitical and policy developments remained key drivers, with major central banks holding rates and emphasising data dependence as inflation moved closer to targets.

Key highlights:

- Markets were constructive but uneven, with a rotation away from US mega-cap growth into value, cyclicals and AI- and commodity-linked markets.

- The US cooled but kept expanding, while Europe and the UK strengthened as inflation moderated.

- Japan outperformed as inflation eased, while China stayed soft and commodities advanced alongside a firmer rand.

Global risk assets posted another broadly constructive month in February, albeit with marked dispersion across regions and styles. Developed market equities, as proxied by the MSCI World Index, returned 0.7% (USD), as investors rotated away from mega cap US technology stocks into value oriented and more cyclically exposed sectors. In contrast, the MSCI Emerging Markets Index gained 5.5% (USD) for the month, supported by strong performance in markets and sectors linked to AI-related infrastructure spending and commodity exporters. Geopolitical and policy developments remained important drivers, with heightened tensions in the Middle East, evolving US trade policy and central banks in major economies keeping policy rates on hold while emphasising data dependence as inflation moved closer to stated targets.

In the United States, data pointed to a cooling but still expanding economy, with Q4 2025 GDP growth slowing to an annualised 1.4% from 4.4% in Q3 as softer consumption and the earlier government shutdown weighed on activity. Headline CPI eased to 2.4% year on year in January 2026, while core CPI stood at 2.5%. On a monthly basis, headline and core inflation rose 0.2% and 0.3% respectively. The unemployment rate edged down to 4.3% as employment increased and labour force participation rose to 62.5%. US equity markets reflected these cross currents, with the S&P 500 down 0.8%, the Nasdaq Composite down 3.3% and the Dow Jones Industrial Average up 0.3% in February 2026 (all in USD). Investors rotated out of software and other growth exposures into value-oriented sectors. Sector performance was highly dispersed, with utilities up 10.4%, energy up 9.5%, and materials up 8.4%, while financials, technology and consumer discretionary fell 3.8%, 3.6% and 3.6% respectively.

Euro area headline inflation slowed to 1.7% in January 2026 from 2.0%, with core pressures also moderating. The European Central Bank kept rates unchanged, with the refinancing rate 2.15% and the deposit rate at 2.00%, signalling that inflation is likely to stabilise near target while avoiding firm guidance on cuts amid growth and geopolitical uncertainty. PMI activity indicators pointed to subdued but expanding momentum, while European equities rallied, with STOXX Europe up 3.7%, supported by diversification away from concentrated US technology leadership. In the UK, CPI fell to 3.0% from 3.4%, while core inflation eased to 3.1%. The Bank of England held Bank Rate at 3.75% in a split vote, noting that inflation remains above target but is trending lower. Growth remained soft but positive. Markets responded constructively, with gilt yields declining by around 25 basis points and the FTSE 100 rising 7.0%, aided by its value-oriented sector exposure.

Japan remained a relative bright spot in global markets. The Nikkei 225 rose 10.4% in February to new highs, driven by rotation into cyclicals, financials and AI-linked semiconductor names. Inflation eased meaningfully, with headline CPI falling to 1.5% and core inflation to 2.0%, moving closer to the Bank of Japan’s target. Activity strengthened, with manufacturing PMI at a four-year high of 52.8, supported by solid domestic demand and resilient exports. The Bank of Japan kept its policy rate unchanged at 0.75%, while longer-dated bond yields edged higher as markets priced in gradual policy normalisation.

In China, macroeconomic conditions remained soft despite ongoing policy support. Headline CPI slowed sharply to 0.2% in January 2026 from 0.8%, while core inflation eased to 0.8%, reflecting weak domestic demand. Manufacturing PMI slipped back into contraction, declining from 49.3 to 49.0 in February, while retail sales showed only modest improvement amid persistent export and investment weakness. The five-year Loan Prime Rate was left unchanged at a record low of 3.50%, signalling continued accommodative policy. Equity performance was mixed, with the CSI 300 marginally positive at 0.2%, while the MSCI China declined 5.5% (USD), as investor sentiment remained cautious around growth momentum and policy effectiveness.

Broader emerging markets, by contrast, fared materially better. The MSCI Emerging Markets index advanced 5.5% (USD) and +4.7% (ZAR), supported by strong returns in Asia, Latin America and other markets benefiting from AI-related capital expenditure themes and elevated commodity prices. Single-country indices such as Brazil’s Bovespa, up around 4.1% in BRL, and India’s Sensex up 0.8% in INR, contributed to the outperformance, highlighting the diversification benefits of exposure to economies less tightly correlated with the US growth and policy cycle.

Commodity markets firmed in February, supported by geopolitical risk premia, solid demand for energy-transition and AI-linked metals, and improved risk sentiment. The broad commodities index rose 1.1%. Brent crude gained +5.1% to USD 72.87/bbl amid tensions in the Middle East, while precious metals outperformed: gold (+7.9%), silver (+10.1%), platinum (+7.9%) and palladium (+4.4%). Industrial metals were mixed, with copper up 1.7% and iron ore down 5.2%.

In foreign exchange markets, the US dollar remained firm on safe-haven demand and higher yields, although expectations for rate cuts persisted. The rand strengthened 0.8% against the dollar, ending the month near R15.92/USD.

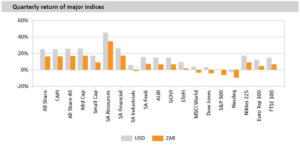

World Market Indices Performance

About RisCura Global monthly market commentary

Explore the retrospective RisCura Global monthly Commentary, spanning vital regions like the USA, UK, Europe, and emerging markets. Gain clarity on economic phenomena with benchmarks on inflation, interest rates, commodity prices, and credit ratings. Tailored for value-driven investors, our insights inform asset allocation across diverse global markets.

Stay informed – subscribe now for insightful perspectives from the RisCura Global Commentary.