Global Market Commentary: January 2026

Risk assets rally as commodities surge and the dollar softens

Global risk assets opened 2026 on a firmer footing, with equities higher across most major regions and emerging markets leading performance amid a softer US dollar. The US macro backdrop remained steady as the Federal Reserve held rates, while cyclical sectors outperformed in equity markets. Commodities and precious metals delivered strong gains, reinforcing a “risk-on” tone despite ongoing policy and geopolitical volatility.

Key highlights:

-

Risk assets strengthened; emerging markets led.

-

US macro steady; Fed held rates.

-

Cyclicals outperformed across equity markets.

-

Commodities rose as the US dollar softened.

Global risk assets recorded a firm start to 2026, with equity performance strengthening across most major regions and styles. The MSCI World Index rose 2.2% in January 2026 (in USD), while the MSCI ACWI gained 3.0% (in USD) and the MSCI Emerging Markets Index advanced 8.9% (in USD). Policy and geopolitical-related volatility remained elevated, against a backdrop of moderating inflation and largely unchanged policy rates across several major economies. Commodities and precious metals advanced during the month, while currency markets reflected a weaker US dollar against several peers.

In the United States, activity data and inflation releases pointed to a steady macroeconomic environment. Headline inflation remained at 2.7% year-on-year in December 2025, with core inflation at 2.6% year-on-year and monthly CPI rising 0.3% in December 2025. The Federal Reserve held the federal funds target range at 3.50%-3.75% at its January 2026 meeting following three interest rate cuts in 2025, noting that inflation remained somewhat elevated. This decision followed a period in which policy rates reached their lowest level since 2022, while labour market indicators continued to point to moderate job gains. The US ISM Manufacturing PMI rose to 52.6 in January 2026, exceeding both the prior reading of 47.9 and the forecast of 48.5, and remaining above the 50-point threshold that separates expansion from contraction. Meanwhile, the 10-year US Treasury yield ended January at 4.26%, above late-2025 levels.

US equity markets delivered positive returns, with the S&P 500 rising 1.5% for the month, supported by broader participation across small cap, mid cap and value segments. Cyclical sectors outperformed including Energy (+14.4%), Materials (8.7%), Industrials (+6.7%) and Communication Services (5.8%). The NASDAQ Composite gained 1.0%, despite earnings related volatility among several large technology stocks, while the Dow Jones Industrial Average rose 1.8%, contributing to a firmer overall US equity backdrop.

In the euro area, economic conditions were characterised by subdued growth and continued disinflation. Consumer inflation eased to 1.9% year-on-year in December 2025, down from 2.1% in November, and below the European Central Bank’s 2.0% target. Energy prices declined 1.9% year-on-year and non-energy industrial goods inflation softened while services inflation moderated and food, alcohol and tobacco inflation edged slightly higher. Against this backdrop, euro area equity benchmarks recorded gains, with the STOXX All Europe Index up 3.5% for the month (in EUR), whilst Germany’s DAX advancing 0.2% (in EUR) while France’s CAC declined 0.3% (in EUR).

In the United Kingdom, consumer price inflation rose to 3.4% year-on-year in December 2025 from 3.2% in November, driven by higher contributions from alcohol and tobacco, transport and food and non-alcoholic beverages. Core inflation remained stable at 3.2% year-on-year, its lowest level since December 2024. UK equity markets advanced over the month, with the FTSE 100 Index gaining 3.0% (in GBP) and moving above the 10 000‑point level for the first time. The gains coincided with steep share price increases in British retailers such as Currys, and Marks & Spencer, as well as advances among precious‑metal miners, defence companies and financial services firms.

Japan’s annual inflation slowed to 2.1% year‑on‑year in December 2025, down from 2.9% in November, while core inflation eased to 2.4% year‑on‑year. The Bank of Japan kept its key short‑term interest rate unchanged at 0.75%, the highest level since 1995. Services activity continued to expand, with the S&P Global Services PMI rising to 53.7 in January 2026 from 51.6 in December 2025, marking a tenth consecutive month above the 50‑point threshold alongside stronger new orders, higher backlogs and increased hiring. Japanese equity markets responded positively, with the Nikkei 225 Index rising 5.9% (in JPY) for the month.

China’s inflation and activity readings remained moderate, with the annual inflation rate rising to 0.8% year on year in December 2025 from 0.7% in November, while core inflation held steady at 1.2% year on year. Housing and transport costs declined while fresh food prices rose. Manufacturing indicators were mixed, with the official PMI falling to 49.3 in January 2026 from 50.1 in December 2025, while the private PMI increased to 50.3. Policy rates remained unchanged, with the one-year Loan Prime Rate at 3.00% and the five-year Loan Prime Rate at 3.50%. Equity markets advanced over the month, with the CSI 300 Index rising 1.8% (in CNY) and the MSCI China Index gaining 4.7% (in USD).

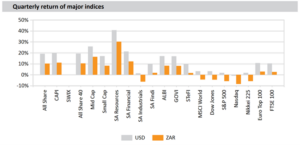

Across emerging markets, the MSCI Emerging Markets Index rose 8.9% (in USD) for the month supported by a risk on global environment and a weaker US dollar. Investor appetite increased for cyclical exposures, alongside stronger performance among small and mid-capitalisation stocks and notable gains in semiconductor related companies. Within individual markets, Brazil’s BVSPA rose 12.6% for the month (in BRL), while India’s SENSEX declined 5.3% (in INR) but remained higher over longer periods.

Commodity markets strengthened in January 2026, with broad-based gains across energy and metals. Oil prices rose 13.9% to $69.32 per barrel, while gold increased 13.3% to $4 894.23 per ounce. Industrial and precious metals also advanced: copper reached $13 067.62 per tonne (+4.9%), platinum $2 195.31 per ounce (+6.5%), silver $85.20 per ounce (+18.9%) and palladium $1 712.50 per ounce (+5.7%). Bulk commodities were mixed, with iron ore slipping to $103.79 per tonne (1.3%) while coal rose to $94.75 per tonne (+9.9%). These movements coincided with firmer energy demand in some developed markets and colder than expected winter conditions in parts of the Northern Hemisphere.

Currency markets reflected a softer US dollar against several peers and firmer emerging market currencies. The rand appreciated 3.2% month-on-month against the US dollar in January 2026, ending the month at R16.04, and the ZAR/GBP rate at R22.11 and the ZAR/EUR rate at R19.15.

World Market Indices Performance

About RisCura Global monthly market commentary

Explore the retrospective RisCura Global monthly Commentary, spanning vital regions like the USA, UK, Europe, and emerging markets. Gain clarity on economic phenomena with benchmarks on inflation, interest rates, commodity prices, and credit ratings. Tailored for value-driven investors, our insights inform asset allocation across diverse global markets.

Stay informed – subscribe now for insightful perspectives from the RisCura Global Commentary.